Why More Sellers Are Hiring a Real Estate Agent

Why More Sellers Are Hiring a Real Estate Agent Some Highlights More homeowners are realizing they need an agent’s help in this complex market – and that’s why a record-lownumber of people are selling without a pro by their side. Without an agent’s help, tackling pricing, staging and repairs, paperw

Read MoreWhat To Expect from the Housing Market in the Second Half of 2026

What To Expect from the Housing Market in the Second Half of 2026 If the first half of this year has left you feeling stuck, you're not the only one. Mortgage rates stayed higher than people wanted. Affordability remained tight. And uncertainty overseas added another layer of pressure nobody saw com

Read MoreLIST WITH BILL & CAY! WE SELL HOMES!

What Buying or Selling a Home Gives Back to Your Community

What Buying or Selling a Home Gives Back to Your Community Buying or selling a home is a big financial decision. And right now, it feels even bigger. Inflation is high, costs are high, and you want to be sure the timing is right before you make your move. But if you do decide to go for it, whether

Read MoreWishing YOU a wonderful 4th of July weekend!

The 1 Factor That Explains Everything Happening with Home Prices Right Now

The 1 Factor That Explains Everything Happening with Home Prices Right Now You've probably heard that home prices are cooling off. And that's true – nationally. But zoom in on individual marketsacross the country, and the picture looks completely different depending on where you are. Some areas are

Read MoreIs It Still a Seller's Market? Here's What the Data Says.

Is It Still a Seller's Market? Here's What the Data Says. Remember a few years back when sellers held all the power and buyers were stuck offering way over asking or waiving inspections just to get a chance at the house? In many markets, those days are behind us. While it’s going to vary by area, mo

Read MoreThe Pricing Mistake That Could Cost You Your Sale

The Pricing Mistake That Could Cost You Your Sale Most sellers come into the market with one number in mind. And it’s often the one that costs them the most. That's their asking price. A survey from Realtor.com shows about 8 in 10 (80%) of sellers expect to sell at or above their asking price today

Read MoreWishing YOU a Wonderful Fathers Day!

Home Prices Are Rising in 71% of Markets

3 Things That Are Not Going To Happen in Today's Housing Market

3 Things That Are Not Going To Happen in Today's Housing Market There’s a lot of uncertainty right now and that’s leading to some dramatic headlines. And if you’re thinking about buying a home, that can make you feel a little less sure about your decision. A recent study by CNBC asked homebuyers wha

Read MoreYOU'RE INVITED NOW ONLY $389,000

Lower Asking Prices Are a Win for Today’s Buyers

Lower Asking Prices Are a Win for Today’s Buyers If affordability has been the biggest thing standing between you and a home, there's a little good news. Asking prices have started to come down. The typical seller listed their house for a median of $429,500 in May. That’s 2.4% lower than a year ago

Read More-

The Mid-Year Housing Market Update: Why Forecasts Changed in 2026

The Mid-Year Housing Market Update: Why Forecasts Changed in 2026 If the housing market feels confusing right now, you’re not alone. Mortgage rates have risen. Home sales haven't picked up like expected. And many buyers and sellers are wondering when things are going to feel easier or be more afford

Read More-

WOW! A 4bdrm home within commuting distance to Boston, Cambridge & Worcester for only $389,000!

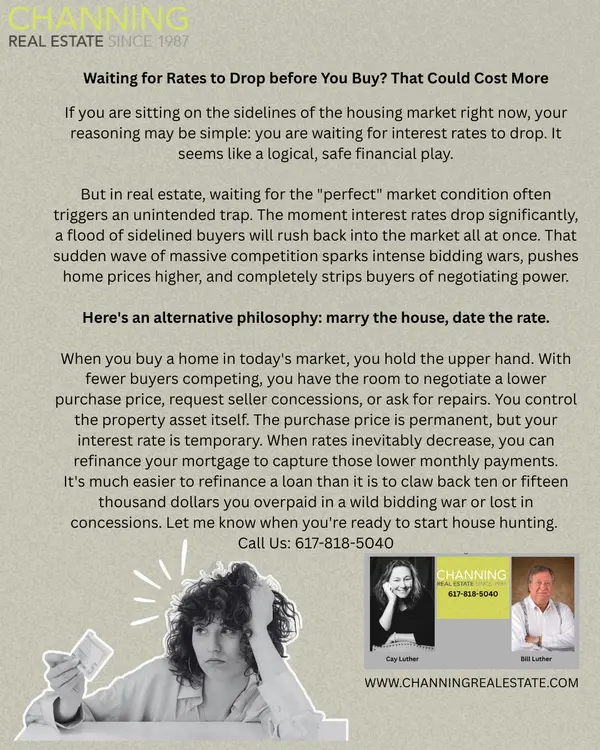

WAITING FOR RATES TO DROP BEFORE YOU BUY? THAT COULD COST MORE!

The Truth About Affordability Today

The Truth About Affordability Today Let's be real with each other for a second about affordability. Because you deserve someone who will be honest and transparent about what’s going on, especially if you’ve got a move on your mind. Here’s the full picture of what’s happening and why. The good – and

Read More-

Why You Don’t Need To Be Afraid of Today’s Mortgage Rates Mortgage rates have been the monster under the bed for a while. Every time they tick up, people flinch and say, “Maybe I’ll wait.” But here’s the twist. Waiting for that perfect 5-point-something rate could end up haunting your wallet later.

Read More

Categories

Recent Posts